For decades, homeowners have wrestled with one of the most challenging questions in property improvement: how much should I actually spend on renovating my home?

Spend too little, and you end up with subpar results that barely move the needle on your property’s value. Spend too much, and you risk pricing yourself out of your neighborhood—making it nearly impossible to recoup your investment when you sell.

The 30% rule has helped countless homeowners navigate the tricky waters of renovation budgeting and avoid one of the most expensive mistakes in real estate: overcapitalization.

What is the 30% rule for renovations? The Complete Answer is provided in this post, enabling you to make informed decisions regarding your property renovation plans.

Affiliate Disclaimer: This post may contain affiliate links, meaning we earn a commission if you purchase through them – at no extra cost to you. We only recommend products or services we believe add value to our readers.

What the 30% Rule Actually Means

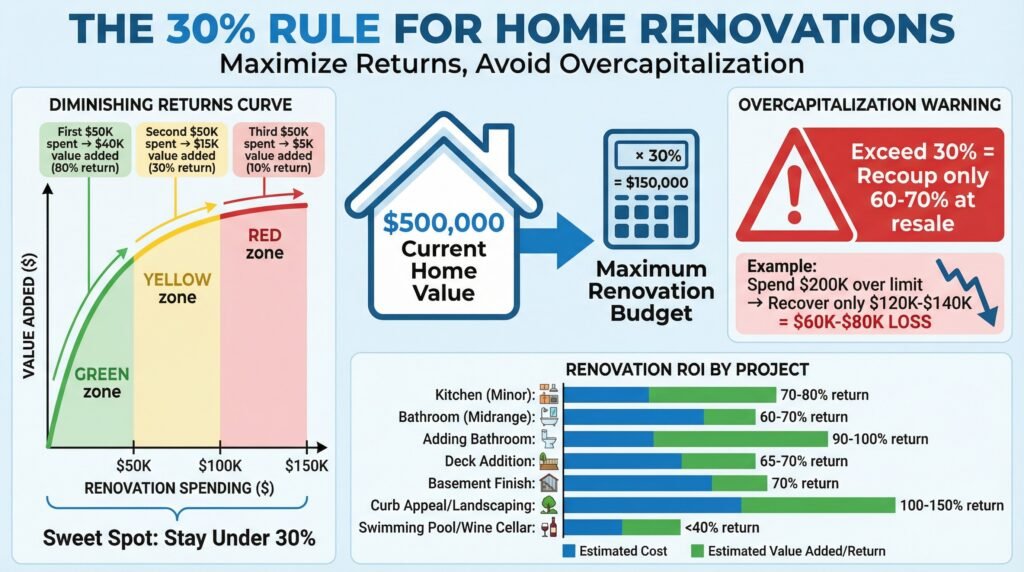

The 30% rule is straightforward in theory. Your total renovation spend should not exceed 30% of your home’s current market value.

If your property is worth $500,000, you shouldn’t pour more than $150,000 into renovations.

Simple enough, right?

This percentage didn’t come from thin air at some real estate conference. The 30% rule emerged from decades of market analysis and post-renovation appraisals, in which industry professionals observed a clear pattern: homeowners who exceeded this threshold rarely realized proportional returns on their investment.

The mathematical reasoning behind this percentage is sophisticated. Property values don’t increase linearly with renovation spending. Instead, they follow a curve of diminishing returns.

The first $50,000 you spend on a dated kitchen might add $40,000 to your home’s value, representing an 80% return.

But that second $50,000 on premium appliances and custom cabinetry might only add another $15,000. By the time you’re installing heated floors and commercial-grade equipment, you’re often adding pennies of value for every dollar spent.

The 30% threshold represents the sweet spot where most homeowners can still expect reasonable returns without venturing into territory where you’re essentially gifting equity to your future buyers.

Understanding Your Home’s True Market Value

Before you can apply the 30% rule, you need to understand what your home is now worth. I’m talking about real value, not what you paid for it, or what Zillow says it might be worth, or what your neighbor thinks properties are going for in the area.

You need an accurate, current market valuation.

Many homeowners stumble right out of the gate by basing their entire renovation budget on outdated or inflated property values, which completely undermines the protective function of the 30% rule.

Getting a professional appraisal is worth the $300 to $500 investment before you start planning major renovations. Appraisers use three main approaches to decide value: the sales comparison approach (looking at recent comparable sales), the cost approach (calculating what it would cost to rebuild), and the income approach (for rental properties).

For most residential properties, the sales comparison approach carries the most weight.

Your appraiser will look at three to five comparable properties, ideally sold within the last six months, within a mile of your home, and similar in size, age, and condition. They’ll make adjustments for differences and arrive at a defensible market value.

Here’s something most homeowners don’t consider: research your neighborhood’s ceiling value. Every neighborhood has one.

This represents the highest price that properties realistically sell for in your area, regardless of how much you invest in renovations.

If the ceiling in your neighborhood is $600,000, and you own a $450,000 home, you’ve only got $150,000 of potential appreciation to work with, no matter how much you spend. This ceiling value should tell your renovation budget even more than the 30% rule in some cases.

Why Overcapitalization Is More Common Than You Think

Overcapitalization happens so many times, and it’s almost never intentional. You decide to renovate your kitchen on a reasonable budget.

But then you’re at the showroom, and you fall in love with those Italian marble countertops.

Then you figure if you’re doing marble countertops, you really should upgrade the cabinets to match. And if you’re doing custom cabinets, it would be silly not to get the premium appliances.

Before you know it, your $40,000 kitchen renovation has ballooned to $85,000.

This phenomenon is so common that contractors and designers have a name for it: scope creep. But there are other, more subtle ways in which overcapitalization happens.

Sometimes it’s geographical.

You might be applying renovation standards from a high-value market to a moderate-value neighborhood. Those design choices that make perfect sense in a $2 million home in San Francisco might be completely out of place in a $400,000 home in a secondary market.

Other times, overcapitalization happens because of emotion. You’re not planning to sell anytime soon, so you justify the spending by thinking you’ll enjoy these upgrades for years.

And that’s fine if you’re renovating for personal enjoyment; the 30% rule becomes less relevant.

But you need to be honest with yourself about whether this is really a “forever home” or whether life circumstances might force a sale in five or ten years.

The data on overcapitalization is sobering. Studies have shown that homeowners who spend more than 30% of their property value on renovations recoup only 60-70% of their investment at resale.

If you spend $200,000 over the 30% threshold, you might only see $120,000 to $140,000 of that reflected in your sale price.

That’s a significant loss of capital that could have been deployed elsewhere.

How to Calculate Your Renovation Budget Using the 30% Rule

Let’s walk through the actual process of applying this rule to your specific situation. Start with your home’s current market value.

Let’s say it’s $450,000.

Multiply that by 0.30, and you get $135,000. That’s your absolute ceiling for renovation spending if you want to stay within this guideline.

But you shouldn’t automatically spend up to that limit. You need to consider several factors that might push your practical budget lower.

First, calculate your neighborhood’s ceiling value.

If comparable homes in your area top out at $550,000, you’ve only got $100,000 of potential appreciation, regardless of what the 30% rule says.

Second, factor in your local market conditions. In a rapidly appreciating market, you might have a bit more flexibility.

In a stagnant or declining market, you should probably aim for 20-25% instead.

Third, consider the age and condition of your home. If you’re working with an older property that needs significant systems updates, like roof, HVAC, electrical, or plumbing, you need to allocate budget to these invisible improvements first.

They don’t add much to resale value, but they’re essential.

This might mean your budget for visible, value-adding renovations is actually much smaller than the 30% rule suggests.

Here’s a practical framework: divide your 30% budget into three tiers. Tier one is essential repairs and updates that bring your home up to market standards.

This might be 40% of your budget.

Tier two is strategic improvements in high-impact areas, usually the kitchen and bathrooms. This might be another 40%.

Tier three is nice-to-have upgrades that improve livability but don’t necessarily drive value.

This is your remaining 20%, and it’s the first thing to cut if you need to scale back.

Link across to perform your calculation with the ‘Home Improvement ROI Calculator’

Strategic Allocation Across Different Renovation Projects

Kitchen renovations typically offer the best return, with minor remodels recouping around 70-80% of costs and major remodels returning 50-60%. But there’s a huge range within “kitchen renovation.” Refacing cabinets, updating countertops, and installing new appliances might cost $25,000 and add $20,000 in value.

Gutting the entire space, moving walls, and installing commercial-grade everything might cost $100,000 and add $50,000 in value.

Bathroom renovations follow a similar pattern. A midrange bathroom remodel typically costs $20,000 to $30,000 and recoups about 60-70% of the investment.

But here’s an insider tip: adding a bathroom often provides better returns than renovating an existing one, especially if your home is bathroom-deficient for its size.

If you have a four-bedroom house with only one bathroom, adding a second bathroom could recoup 90-100% of costs because you’re fixing a basic deficiency.

Outdoor improvements represent an interesting category. Deck additions typically recoup about 65-70% of costs.

But landscaping is trickier.

Basic improvements offer excellent returns, often 100-150% for simple curb appeal upgrades, while elaborate landscaping offers poor returns. A $5,000 investment in fresh mulch, new plantings, and lawn care might add $7,500 in value.

A $50,000 investment in an elaborate hardscape might add only $25,000.

Basement finishing offers moderate returns of about 70%, but only if your market values finished basements. In some areas, buyers see basements as storage space regardless of finish level.

Do your homework on local preferences.

Here’s what rarely pays off: swimming pools (except in very specific markets), luxury upgrades like wine cellars or home theaters, highly personalized spaces like elaborate home gyms, and over-improving for your neighborhood. That last one is crucial.

If you’re the only house on the block with an $80,000 kitchen renovation, you won’t get full value for it because your neighborhood’s comps don’t support it.

Adjusting the Rule for Different Property Types and Markets

For investment properties, you should be more conservative and aim for 20-25% rather than 30%. Investment properties are evaluated on cash flow and cap rates, not emotional appeal.

Spending beyond basic functionality rarely translates to proportionally higher rents.

If a property generates $2,000 per month in rent with $20,000 in renovations, it might only generate $2,200 per month with $40,000 in renovations. That extra $200 doesn’t justify the extra capital outlay.

In luxury markets, the rules become more flexible and complex. High-end buyers expect certain finishes and features, so skimping actually costs you more than overspending.

But the 30% threshold might stretch to 40% or even 50% in markets where properties routinely sell for multiples of their pre-renovation values.

The key is understanding the specific expectations of luxury buyers in your market.

For historic homes, you’re dealing with a different calculation entirely. Renovations must often meet preservation guidelines, which substantially increase costs.

But historic properties can also command significant premiums if renovated sensitively.

You might spend 40% of the current value on a renovation and see 100% of that reflected in increased value because you’re appealing to a specific buyer pool that values authenticity and craftsmanship.

In rapidly appreciating markets, you have more room to push the boundaries. If your market is appreciating at 10% annually, a renovation that exceeds 30% today might be perfectly reasonable within two years as your property value rises.

But be careful with this logic.

Markets can turn quickly, and you don’t want to be caught with an over-improved property when appreciation slows or reverses.

In declining or stagnant markets, you should be much more conservative. Aim for 15-20% at most, and focus exclusively on repairs and updates that prevent value loss rather than improvements that add value.

In these markets, you’re playing defense.

Financing Considerations Within the 30% Framework

How you finance your renovation dramatically impacts whether the 30% rule makes sense for your situation. If you’re paying cash, the 30% rule applies most directly.

You’re risking that capital against the potential increase in property value, and you need to ensure you’re not overcapitalizing.

But if you’re financing the renovation, you need to factor in borrowing costs. Let’s say you take out a home equity line of credit at 7% interest for a $100,000 renovation on your $400,000 home.

That’s 25% of your home’s value, well within the 30% guideline.

But if this renovation only adds $80,000 in value, and you’re paying $7,000 per year in interest, you’re actually losing money every year you don’t sell.

Here’s a framework for thinking about financed renovations: calculate your all-in cost, including interest over a realistic holding period. If you plan to sell in three years, and your renovation costs $100,000 plus $21,000 in interest, your real cost is $121,000.

Now apply the 30% rule to that number.

Does it still make sense?

Cash-out refinancing presents another consideration. If you refinance to pull out equity for renovations, you’ll permanently increase your monthly payment.

That reduced cash flow needs to be worth it.

Calculate how much extra value the renovation needs to add just to break even on the increased mortgage payment over your expected holding period.

Some homeowners use FHA 203(k) loans or similar renovation loans that finance both the purchase price and renovation costs into a single mortgage. These can be excellent tools for buying undervalued properties and renovating them to market standards.

But they can also tempt you to over-improve because the money feels “free” when it’s rolled into a 30-year mortgage.

It’s not free. You’re paying interest on it for three decades.

Financed renovations need a lower threshold for value addition to make financial sense. If you’re paying cash, you might be comfortable with a renovation that adds 70% to its cost in value.

If you’re financing at 7% for 10 years, you might need that renovation to add 90% of its cost in value just to break even.

Tracking Costs and Avoiding Budget Overruns

Start by getting multiple detailed bids for your renovation work. I mean line-item bids that break down materials, labor, permits, and fees.

This transparency helps you see exactly where your money is going and where you might be able to make strategic cuts if needed.

Build in a contingency fund of at least 15-20% of your total budget. Unexpected issues arise in almost every renovation, especially in older homes.

That water damage behind the shower tile you’re replacing, the outdated electrical that needs upgrading to meet current code, and the termite damage in the floor joists.

These surprises can quickly blow through thousands of dollars if you haven’t planned for them.

Track your spending in real time. Use a spreadsheet or project management app to log every expense as it occurs.

Compare your actual spending against your budget weekly.

This real-time tracking helps you catch budget creep early when you can still make adjustments.

Understand the difference between cost overruns and scope changes. A cost overrun occurs when the work you planned to do costs more than expected. A scope change is when you decide to do extra work beyond your original plan.

Most renovation budget disasters involve scope changes.

That decision to add a powder room while you’re already renovating the first floor, or to upgrade to hardwood instead of laminate flooring. These scope changes can push you beyond the 30% threshold before you realize it.

Establish decision gates throughout your project. These are predetermined points at which you assess your budget status and decide whether to proceed with optional upgrades.

Maybe after the rough-in is finished, you can evaluate whether you can afford those upgraded light fixtures.

After cabinetry is installed, you decide whether the budget allows for the decorative backsplash you’ve been considering. This structured approach prevents the drift toward overcapitalization.

When to Ignore the 30% Rule

If you’re truly renovating for the long term and have no plans to sell within the next 10-15 years, the rule becomes less relevant. Your focus shifts from maximizing resale value to maximizing personal utility and enjoyment.

You might spend 50% of your home’s value creating your dream kitchen because you’ll use and enjoy it for 15 years.

The financial return matters less than the quality-of-life return.

When you’re correcting serious deficiencies or safety issues, you need to spend what’s necessary regardless of the 30% threshold. A failing foundation, extensive mold remediation, finish roof replacement, or total electrical system upgrade.

These aren’t optional, and not addressing them will cost you more in the long run, either through continued deterioration or reduced marketability.

In extremely competitive markets where bidding wars are common, strategic over-improvement might make sense. If spending 35% instead of 30% on renovations means your home will stand out and sell for a premium in a hot market, the math might work out.

But this requires really good market intelligence and timing.

If you’re planning a house hack or conversion to a rental property, different metrics apply. You might spend 40% of the current owner-occupied value on renovations to convert a single-family home into a legal duplex, knowing that rental income and the value as an investment property will provide returns through a mechanism other than simple resale value appreciation.

Forced renovations because of insurance or code requirements also fall outside the 30% framework. If your insurance company requires specific updates or your municipality mandates compliance with new building codes, you don’t really have a choice.

The key distinction is intentionality. If you’re deliberately exceeding 30% for strategic reasons and understand the financial implications, that’s a defensible choice.

If you’re exceeding 30% because you lost track of spending or got caught up in the excitement of renovation choices, that’s a problem.

People Also Asked

How much should I spend renovating my home?

Generally, your total renovation spending should stay below 30% of your home’s current market value. For a $400,000 home, that means keeping your renovation budget under $120,000.

This threshold helps prevent overcapitalization, where you spend more on improvements than you can recover when selling.

The exact amount depends on your neighborhood’s ceiling value, local market conditions, and whether you plan to sell soon or stay long-term.

What happens if I spend too much renovating my house?

Spending beyond 30% of your home’s value typically results in overcapitalization. Studies show homeowners who exceed this threshold recoup only 60-70% of their investment at resale.

If you spend $200,000 over the recommended limit, you might only see $120,000 to $140,000 of that reflected in your home’s sale price.

You essentially gift equity to your future buyers rather than building wealth for yourself.

Does a kitchen renovation add value to my home?

Kitchen renovations typically add 50-80% of their cost back to the home’s value, depending on the scope. A minor kitchen remodel costing $25,000 might add $20,000 in value, while a major gut renovation costing $100,000 might only add $50,000 to $60,000.

The first dollars you spend provide the best return.

Premium upgrades like commercial-grade appliances and custom cabinetry often add minimal value compared to their cost.

Should I renovate my house before selling?

The decision to renovate before selling depends on your home’s condition relative to comparable properties in your neighborhood. If your home is significantly dated or has obvious deficiencies, such as an outdated kitchen or only one bathroom in a four-bedroom house, strategic renovations can pay off.

However, major renovations that exceed 30% of your home’s value rarely make financial sense if you’re selling soon.

Focus on repairs that bring your home up to market standards rather than luxury upgrades.

How do I calculate my neighborhood’s ceiling value?

Research recent sales of the highest-priced homes in your immediate neighborhood, ideally within half a mile of your property. Look at homes sold in the past six months that represent the upper limit of what buyers will pay in your specific area.

This ceiling value represents your most potential home value regardless of how much you spend on renovations.

If your neighborhood’s ceiling is $600,000 and your home is worth $450,000, you have at most $150,000 of potential appreciation to work with.

Are bathroom renovations worth the investment?

Midrange bathroom renovations typically recoup 60-70% of their cost, with projects averaging $20,000 to $30,000 in spending. Adding a bathroom often provides better returns than renovating an existing one, especially if your home is short on bathrooms.

A four-bedroom house with only one bathroom could see a 90-100% return on adding a second bathroom because you’re fixing a basic problem that limits your home’s marketability.

What renovations should I avoid?

Swimming pools rarely add value except in specific warm-weather markets. Luxury additions like wine cellars, home theaters, and elaborate home gyms appeal to narrow buyer segments and typically recoup less than 40% of their cost.

Highly personalized renovations and over-improving beyond your neighborhood’s standards also provide poor returns.

If you’re the only house with $80,000 worth of upgrades on a block where homes sell for $400,000, you won’t recoup that investment.

Key Takeaways

The 30% rule prevents overcapitalization by limiting renovation spending to 30% of your home’s current market value, helping you avoid spending more than you can recover at resale.

Start with an accurate professional appraisal of your home’s current value and research your neighborhood’s ceiling value, as this often matters more than the mathematical 30% calculation.

Kitchen and bathroom renovations typically offer the best returns at 50-80% of cost, while luxury upgrades and highly personalized improvements often recoup less than 40%.

Adjust the rule based on your situation: be more conservative for investment properties (20-25%) and declining markets, while allowing slightly more flexibility in luxury markets and owner-occupied homes where you’ll stay for 10-plus years.

Factor in total financing costs when calculating whether a financed renovation makes sense, as interest payments over time can turn a seemingly good investment into a money-losing proposition.

Build a 15-20% contingency fund into every renovation budget and track spending weekly to catch scope creep before it pushes you beyond the 30% threshold.

The rule can be ignored when renovating a true forever home where you’ll live for 10-15 years, correcting serious safety issues, or executing strategic plans that generate returns from rental income rather than resale value.

Long-term value creation comes from consistent maintenance spending 2-3% of home value annually, which protects and enhances value while staying well within the 30% threshold over any reasonable time period.

Leave a Reply