Herewith, a detailed answer to the question: What is the 70 percent Rule in House Flipping?:

The 70 % rule in house flipping is a formula that helps real estate investors decide the maximum price to pay for a distressed property while ensuring profitability.

Consider walking through a distressed property with dollar signs in your eyes. The place has good bones, the neighborhood is solid, and you can already picture the gleaming hardwood floors and updated kitchen.

You’ve got the contractor’s repair estimate, the seller seemed motivated, and you’re ready to make an offer.

Then your mentor asks you one simple question: “Did you run the 70% rule?”

You did not. When you did, you realized you’re about to overpay by nearly $40,000.

That cold splash of mathematical reality can save you from what would have been a disastrous flip.

The 70% rule states that you shouldn’t pay more than 70% of the property’s after-repair value minus repair costs. This formula emerged from decades of real-world flipping experience, accounting for all the expenses that beginners consistently underestimate or forget entirely.

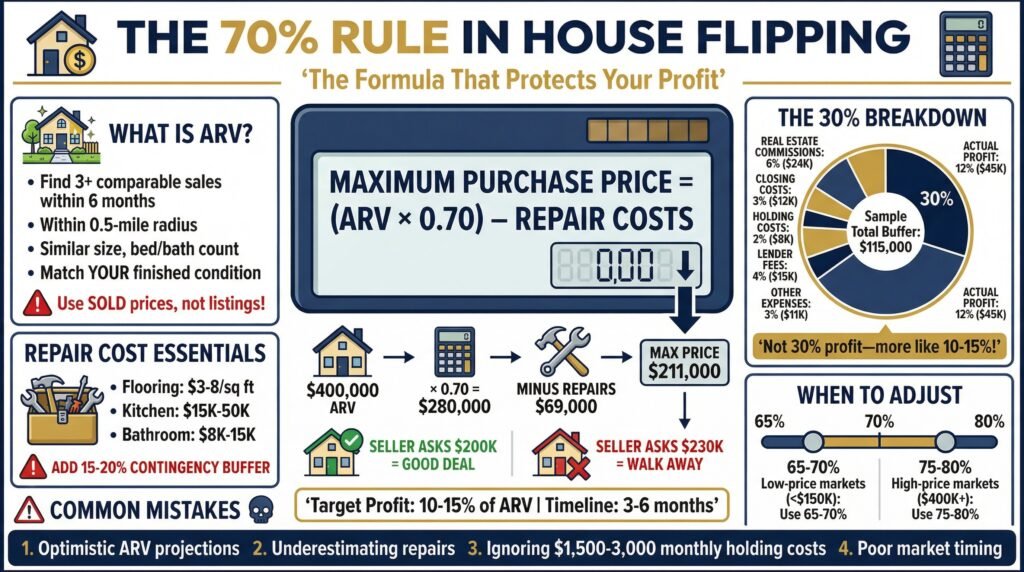

Here’s what you’re working with: (ARV × 0.70) – Estimated Repair Costs = Maximum Purchase Price

That ARV is your after-repair value, the price the property will realistically sell for once you’ve completed all renovations. The 0.70 represents keeping 30% of the ARV available for everything else.

And those estimated repair costs need to be honest, detailed, and padded for the inevitable surprises.

Let’s get one thing straight right now. That remaining 30% represents your buffer for all transaction costs, holding expenses, and profit combined. Too many new flippers make the mistake of thinking they’re walking away with nearly a third of the property value as pure earnings.

That 30% has to cover agent commissions on both ends of the deal, closing costs twice, title insurance, property taxes during your holding period, utilities while the place sits empty, insurance, hard money lender fees and interest, staging costs, marketing expenses, transfer taxes, and about a dozen other things that add up faster than you’d believe.

Affiliate Disclaimer: This post may contain affiliate links, meaning we earn a commission if you purchase through them – at no extra cost to you. We only recommend products or services we believe add value to our readers.

Understanding After-Repair Value

The ARV calculation determines whether most deals will succeed or fail. You can have the best renovation crew in town and stay under budget, but if you overestimated what buyers will actually pay for the finished product, you’re toast.

Spend more time researching ARV than any other aspect of a potential flip. You need recently sold properties, not ones listed now.

Listings show you what sellers hope to get.

Sold comparables show you what buyers actually paid. There’s often a significant gap between those two numbers, sometimes as much as 5% to 10% in slower markets.

Look for properties within a half-mile radius that sold in the last 3 to 6 months. They should match your subject property’s square footage within about 10%, have the same number of bedrooms and bathrooms, and most importantly, be in similar condition to what yours will be after renovation.

That last part trips people up all the time. You can’t compare your future renovated property to the current distressed sales in the neighborhood.

You need to find the nice, recently updated sold homes.

If you’re planning granite countertops and hardwood floors, your comparables should have granite countertops and hardwood floors.

Talk to local real estate agents who specialize in the neighborhoods you’re targeting. These conversations reveal things the data doesn’t show.

Maybe a new Amazon distribution center is opening, driving demand.

Perhaps a major employer just announced layoffs. The local school district might be redistricting, which dramatically affects property values.

This qualitative information adjusts your ARV up or down from the raw comparables.

Market timing matters more than people admit. In a red-hot seller’s market, you might confidently use ARV estimates at the higher end of your comparable range.

In a cooling market or during economic uncertainty, you’d better use conservative numbers from the lower end.

Rather leave $10,000 on the table than get stuck holding a property that won’t sell at your projected price.

One recommended technique is to create three separate ARV scenarios for each property: conservative, moderate, and optimistic. Your conservative estimate uses only the lower-end comparables and assumes a slower market.

Your moderate estimate uses the middle range of comparable sales.

Your optimistic estimate uses the higher-end sales but only when market conditions strongly support them. If a deal doesn’t work even with your optimistic ARV, pass immediately without further analysis.

Estimating Repair Costs Accurately

Your estimated repair costs need to be ruthlessly realistic. This is where bringing in actual contractors becomes non-negotiable.

Get written estimates from licensed professionals for any significant work, especially foundation issues, roof replacement, electrical upgrades, or plumbing overhauls.

For cosmetic renovations, you develop a sense of costs after a few projects. New flooring typically runs between $3 and $8 per square foot, depending on the materials.

Kitchen renovations can range from $15,000 for a basic refresh with new cabinets and countertops to $50,000 for high-end full remodels.

Bathroom updates usually fall between $8,000 and $15,000 per bathroom.

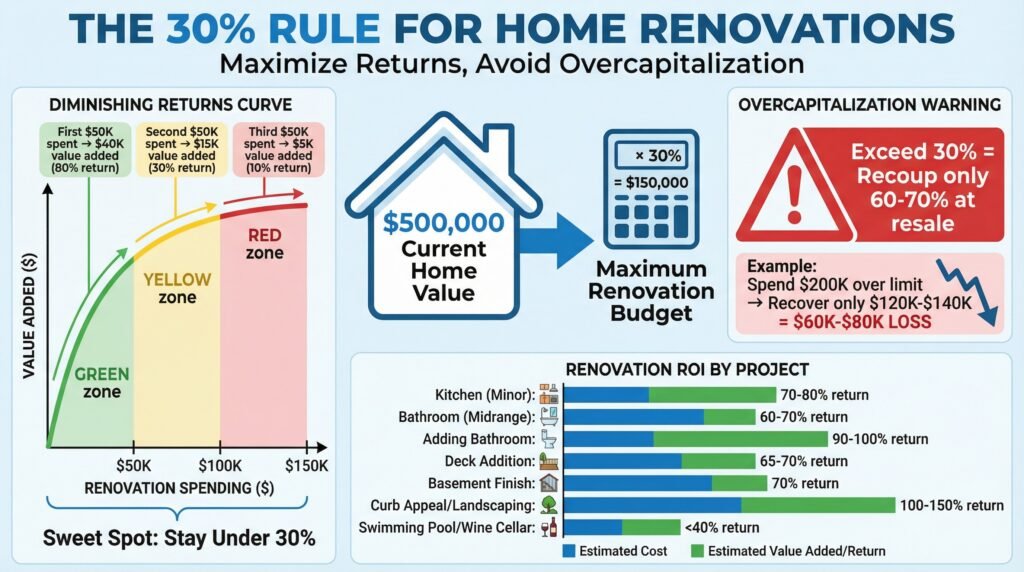

But here’s the thing that separates successful flippers from the ones who wash out after their first deal. You absolutely must add a contingency buffer of 10% to 20% to your repair estimates.

Use 15% as your standard buffer, and bump it to 20% for properties built before 1970 or anything that’s been vacant for over a year.

Why such a large buffer? Because homes hide problems.

That water stain on the ceiling might show a simple roof leak, or it might reveal extensive rot in the roof decking that needs replacing half the roof structure.

Those outdated electrical outlets might just need swapping, or you might explore knob-and-tube wiring throughout the entire house that needs a complete rewiring job. The foundation might look fine until you start work and realize there’s significant settling that needs to be addressed.

Also, account for holding costs in this planning phase. Every month, owning the property costs money.

Property taxes don’t stop. Insurance premiums are due. If you’re using hard money financing, that interest accrues daily. Utilities need to stay on so contractors can work and potential buyers can view the property.

These monthly carrying costs typically run $1,500 to $3,000, depending on the property, and they eat directly into your profit margin. A property that was supposed to flip in three months but actually takes six months has just consumed an extra $4,500 to $9,000 in holding costs that might wipe out a significant chunk of your expected profit.

A hard lesson to learn in house flipping:

The contractor promised a two-month timeline for what seemed like straightforward cosmetic work. Four months later, you’re still working on the property because he kept discovering new issues, and his crew was pulled to other jobs. Those extra two months can be costly, with additional holding expenses that weren’t properly budgeted for.

Applying the 70% Rule in Real Scenarios

Let me walk you through how this actually works when you’re standing in a property trying to decide whether to make an offer.

You find a distressed property in a solid neighborhood. You research comparable sales and decide the ARV will be $400,000 once renovations are finished.

Your contractors have provided written estimates totaling $60,000 for all necessary repairs.

You add your 15% buffer, bringing repair costs to $69,000.

Now you run the calculation: $400,000 × 0.70 = $280,000. Then subtract your repair costs: $280,000 – $69,000 = $211,000.

That’s your maximum purchase price.

If the seller wants $230,000, you walk away. The numbers don’t work.

If the seller will take $200,000, you’ve got a deal that follows the formula and leaves room for the inevitable cost overruns and market fluctuations.

Let’s look at what that remaining 30% actually covers in this scenario. Your ARV is $400,000, so 30% equals $120,000.

Your purchase price is $211,000, and repairs are $69,000, totaling $280,000.

That leaves $120,000 before profit.

From that $120,000, you’re paying roughly 6% in combined real estate commissions ($24,000), closing costs on purchase and sale (approximately $12,000 combined), title insurance and escrow fees ($4,000), property taxes for six months of ownership ($6,000), insurance ($2,000), utilities during construction and listing ($1,500), hard money lender fees and interest ($15,000), staging ($3,000), photography and marketing ($1,000), transfer taxes ($2,500), and miscellaneous expenses ($4,000). That totals about $75,000 in extra costs.

Your actual profit on this deal is $45,000, not $120,000. That represents an 11.25% return on the ARV, which is respectable but nowhere near the 30% that beginners mistakenly calculate as pure profit.

When to Adjust the 70% Rule

The 70% rule needs to be adjusted based on your specific market conditions and circumstances. This formula serves as a guideline, not an absolute law carved in stone.

In lower-priced markets where ARVs typically fall below $150,000, you may need to be more conservative, potentially using 65% rather than 70%. Your fixed costs don’t scale down proportionally with cheaper properties.

Title insurance, attorney fees, and inspection costs are similar whether you’re flipping a $100,000 property or a $300,000 property.

These fixed costs consume a larger percentage of your margin on cheaper properties.

Conversely, in higher-priced markets where ARVs exceed $400,000, you might be able to stretch to 75% or even 80% in some cases. Those fixed costs take up a smaller share of the overall deal, leaving more room in your budget.

Your local market competition also dictates adjustments. Try to flip properties in a hot market where institutional investors and well-funded flippers are making aggressive offers.

Sticking rigidly to 70% will mean that you cannot win any deals.

Adjust your rule to 75% and accept thinner profit margins, but be extremely conservative with ARV estimates and get multiple contractor bids to confirm that your repair costs are rock-solid.

If you’re a licensed real estate agent doing your own flips, you’ve got a built-in advantage. You save the buyer’s agent commission when purchasing (typically 2.5% to 3%) and the listing agent commission when selling (another 2.5% to 3%).

That’s a combined 5% to 6% savings that lets you pay more for properties while maintaining the same profit margins as investors using agents.

Your exit strategy fundamentally changes the math, too. The 70% rule is designed specifically for fix-and-flip scenarios where you sell within 6 to 12 months.

If you’re planning a buy-and-hold rental strategy, you can typically afford to pay 75% to 80% of ARV because you’re not immediately reselling.

Your returns come from cash flow, loan paydowns, and long-term appreciation rather than a quick flip profit.

Common Mistakes That Kill Deals

The biggest mistake that keeps happening is optimistic ARV projections. Beginners fall in love with a property’s potential and start using aspirational comparable sales instead of realistic ones.

They’ll look at the nicest house in the neighborhood that sold for top dollar and assume their renovation will achieve the same price.

More often, you’ll end up somewhere in the middle of the comparable range, not at the top.

Another killer is underestimating the scope of repairs during your initial walkthrough. You see cosmetic damage and price out cosmetic fixes, but you don’t investigate deeply enough to explore the structural, electrical, or plumbing issues hiding behind those walls.

Bring an experienced contractor to every property you’re seriously considering.

That $200 payment for their time and expertise will save you from countless bad deals.

Ignoring holding costs is remarkably common. New flippers calculate purchase price and repair costs, but forget that every single month of ownership drains resources.

If your renovation takes four months instead of two, that’s an extra $6,000 to $10,000 in carrying costs.

If the property sits on the market for three months instead of selling in 30 days, another $9,000 to $12,000 is gone.

Market timing misjudgments have burned plenty of investors.

Example: Your projected ARV of $350,000 become a realistic selling price of $320,000. You’re lucky and still make a small profit, but only because you’ve been conservative with repair estimates and the property sold quickly.

Some investors also make the mistake of using the 70% rule as their only analysis tool. The formula serves as a starting point for determining whether a deal merits deeper investigation.

You still need to research neighborhood crime rates, school district quality, employment trends, future development plans, and a dozen other factors that affect both your ability to sell and the price buyers are willing to pay.

Building Your Systematic Approach

The 70% rule becomes more valuable when you systematize your entire evaluation process. Use a standardized spreadsheet for every potential property, requiring you to account for all expense categories.

Your spreadsheet includes fields for purchase price, estimated repair costs by category, ARV based on three different comparable scenarios (conservative, moderate, optimistic), holding period estimates, financing costs, all closing expenses, commission structures, and contingency buffers. Run three scenarios through the formula using the conservative ARV, moderate ARV, and optimistic ARV.

If the deal doesn’t work even with the optimistic ARV projection, immediately pass. This systematic approach removes emotion from decision-making.

Walk away from properties, no matter what, if the numbers don’t support the 70% rule.

Track every deal you assess, whether you purchase it or not. This database lets you analyze the accuracy of your ARV estimates over time.

You’ll learn if you tend to be about 3% to 4% optimistic in your ARV projections, so you can intentionally reduce your estimated ARV by 4% before running the 70% formula. Conversely, you’ll learn if you’re generally too conservative and need to adjust your ARV accordingly.

This personal correction factor will significantly improve your actual profit margins.

The most successful flippers I know have similar systems. They’ve identified their own patterns, biases, and market-specific factors that require adjustments to the formula.

They’ve calculated their actual expense ratios across many projects and know whether they need 28%, 30%, or 32% of ARV to cover costs and achieve their target profit margins.

Frequently Asked Questions

Can I flip a house with $50,000?

You can flip a house with $50,000 in certain markets, particularly lower-priced areas where property values are under $150,000. However, you’ll need to use the $50,000 as a down payment with hard money financing or partner with someone who can provide extra capital.

The $50,000 alone won’t cover purchase, repairs, and all associated costs on most properties.

How much profit should you make on a house flip?

Most successful flippers target profits between 10% and 15% of the after-repair value. On a $300,000 property, that means a profit of $30,000 to $45,000.

Anything less than 10% doesn’t provide enough buffer for unexpected issues, and projecting more than 15% often means you’re being overly optimistic with your numbers.

What is the 80% rule in real estate?

The 80% rule is a more aggressive version of the 70% rule that some experienced investors use in lower-cost markets or when they have competitive advantages, such as being a licensed agent or having an in-house construction crew. Using 80% instead of 70% reduces your profit margin and safety buffer, making it suitable only for investors with extensive experience and accurate cost estimation abilities.

How do you calculate the after-repair value for a flip?

Calculate ARV by finding at least three comparable properties that sold within the last six months, within half a mile of your subject property, with similar square footage, bedroom and bathroom counts, and condition to what your property will be after renovation. Average these sale prices and adjust up or down based on any significant differences between the comparables and your subject property.

Is house flipping still profitable in 2026?

House flipping remains profitable in 2026 but requires greater discipline and conservative estimates than during the low-interest-rate environment of previous years. Higher borrowing costs, increased material and labor expenses, and more volatile market conditions mean you need to be more selective about which deals you pursue and more conservative with your ARV projections.

How long should a house flip take?

Most house flips should be completed within three to six months from purchase to sale. Renovation work typically takes 2 to 4 months, depending on the scope, followed by 1 to 2 months on the market.

Every month beyond six months significantly eats into your profit through holding costs and increases your risk of market condition changes.

What are typical holding costs for a flip?

Typical holding costs range from $1,500 to $3,000 per month and include property taxes, insurance, utilities, loan interest, HOA fees (if applicable), security monitoring, lawn maintenance, and winterization expenses. These costs vary significantly by property value, location, and financing terms, but should always be included in your total project expenses.

Key Takeaways

The 70% rule provides mathematical certainty that profit potential exists before you purchase a property. The formula is (ARV × 0.70) – Repair Costs = Maximum Purchase Price.

That 30% buffer covers all expenses beyond purchase and repairs, commissions, closing costs, holding expenses, and financing charges, with your actual profit typically ending up between 8% and 15% of ARV on successful flips.

ARV accuracy determines everything because every other calculation depends on it. Use conservative estimates based on recently sold comparable properties, not aspirational projections or current listings.

Always include a 15% to 20% contingency buffer on repair estimates because homes hide problems that only reveal themselves once work begins.

Adjust the percentage based on your market conditions, property price point, and personal circumstances. Lower-priced properties might require 65%, while higher-priced properties in strong markets might support 75% to 80%.

The rule serves as a guideline that needs to be customized to your specific situation, not a rigid formula that works identically everywhere.

Leave a Reply